Family Banking: The Growth Strategy Financial Institutions Are Missing

Money is managed as a family. Your banking experience should be too. Here’s how family banking drives engagement, retention, and growth.

Most financial institutions still design products for individuals. But that’s not how money really works.

Real financial decisions happen in families. A teen saving for a first car. Parents guiding everyday financial decisions. Adult children supporting aging parents. Money is talked about, planned, and managed together, across the household.

Family banking is about recognizing that reality. It’s a shift from thinking in individual accounts to thinking in connected financial relationships.

What Is Family Banking? 🏦

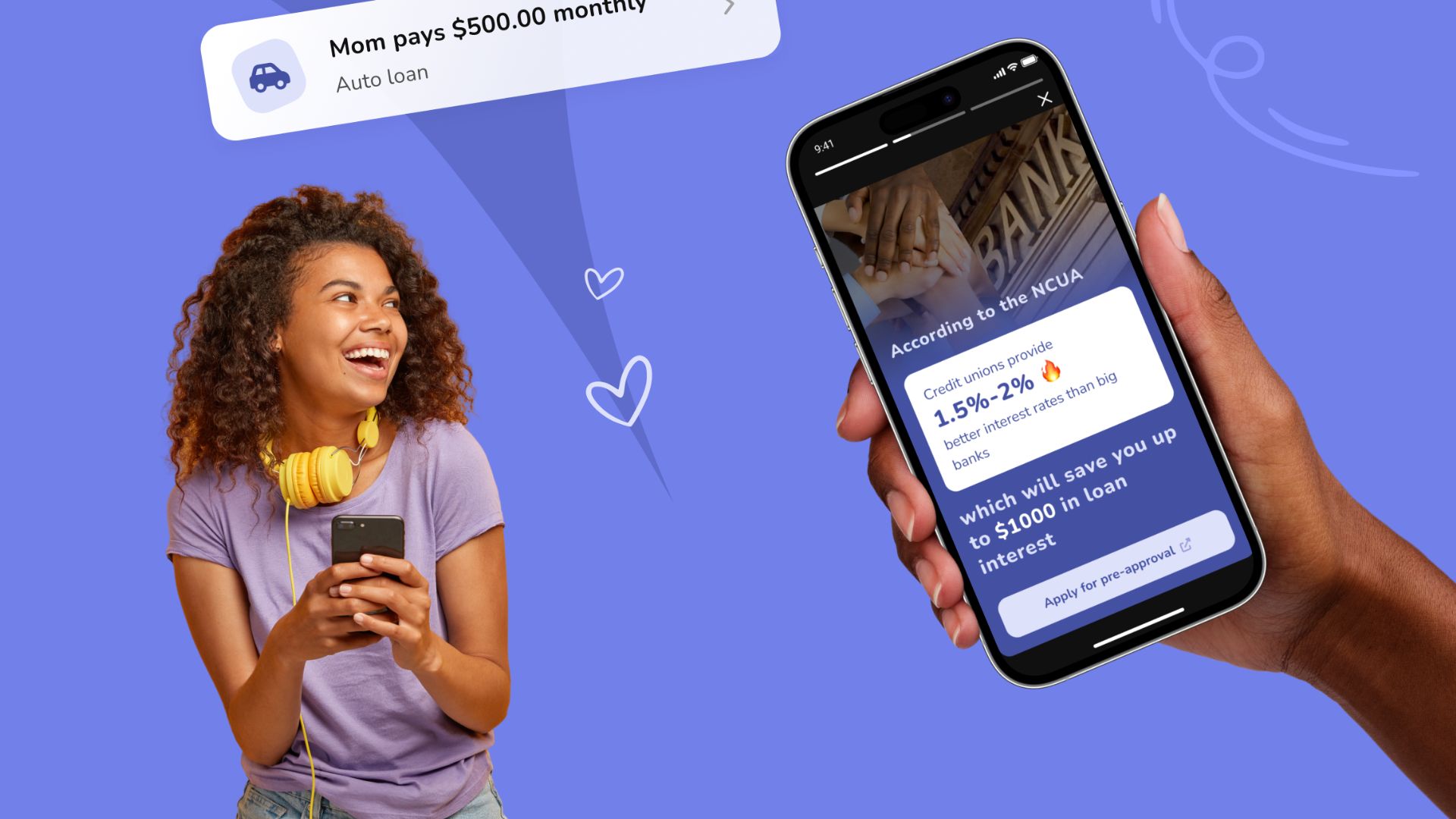

Family banking is about helping families manage money together, not separately. Instead of treating each person like their own silo, it brings parents, kids, and the whole household into one shared experience.

No more jumping between apps or logins. Everything lives in one place. Parents can guide and support. Kids learn how money actually works. And those everyday moments turn into real financial habits.

At the end of the day, it’s about being there for the whole family, making money feel simpler, more transparent, and a lot more collaborative.

Family Banking vs. Youth Banking 👨👩👧👦

Many institutions believe they’re already doing this through youth accounts, but the two aren’t the same.

Youth banking focuses on a segment.

It’s built for kids or teens, often as standalone products.

Family banking focuses on relationships.

It connects parents, children, and even extended family into one cohesive experience.

Youth accounts can help with early engagement. But without the broader family context, they often don’t turn into long-term relationships or deeper product adoption.

Family banking creates continuity:

- From a first allowance

- To a first savings goal

- To a first major financial decision

All within the same institution.

Why This Shift Matters for Growth 📈

The race for younger customers starts way before 18, and most traditional institutions aren’t winning it.

Millennial parents are shaping how kids learn about money. They want simple, intuitive tools that fit real life. So families are turning to fintechs that show up early, around allowance, saving, and first purchases.

By the time banks step in, the habits (and trust) are already built somewhere else.

That leads to:

- Missed early engagement

- Weaker household relationships

- Lower long-term value

Family banking helps close that gap, so institutions can show up earlier, stay relevant longer, and grow with the family.

From Accounts to Relationships 🔄

Family banking isn’t just a set of features. It’s a shift in how institutions think about growth.

It means moving from:

- Products → Journeys

- Users → Households

- Transactions → Relationships

The institutions that win in the next decade won’t just offer better products. They’ll be the ones that show up for the moments that matter, from the first dollar saved to the first major financial decision.

How Boucoup Enables Family Banking

Boucoup is a family banking platform built for banks and credit unions that want stronger, more consistent engagement across the household, not just one user at a time.

It integrates directly into your existing digital banking experience, so families stay engaged inside your ecosystem instead of drifting to third-party apps.

With Boucoup, institutions can:

- Offer connected experiences for parents and children

- Support real-life financial journeys like saving, spending, and milestones

- Deliver guidance and product offers at the right moments

- Keep deposits, relationships, and engagement within the institution

Final Thought

If fintechs are winning early, it’s not because they have better products. It’s because they’re showing up earlier.

Family banking is how financial institutions catch up and turn early moments into lasting relationships.

Want to learn more? Let’s talk about how this strategy can work for your institution.

Welcome to our blog on all things BankingON and our perspective on what's going on in the Credit Union and Banking Industry. If you get a chance, share our posts on social media!

Featured Posts